Su carrito está vacío

Carrito

If your budget feels tight even when you’re doing “everything right,” this might surprise you.

I’m a financial therapist, and a few years ago, I challenged myself to cut $4,000 from my annual spending—without touching the things that make life enjoyable.

I didn’t cancel Netflix. I didn’t stop eating out. I didn’t stop living. Instead, I found five weird leaks hiding in plain sight.

I’m Sarah Chen, CFP. After 12 years helping clients fix their money habits, I realized the most powerful savings come from invisible expenses—the ones that quietly drain your account while you think you’re being responsible.

These are the five things I cut that actually worked (and no, none of them involve coffee).

I found $612 a year in random subscriptions—apps, software, a “free trial” from 2021 that still billed me. I set a reminder to check renewals every quarter and canceled eight services in 15 minutes.

Saved: $612/year

My car insurance, Amazon Prime, and gym renewal always blindsided me. I wasn’t overspending—I was under-planning. I started splitting those into mini-monthly amounts inside my budget by paycheck.

Saved: $780 in late fees and interest charges

I unsubscribed from 23 brand newsletters. Suddenly, I stopped “rewarding myself” with $40 orders that didn’t matter. The urge vanished once I stopped seeing the temptation.

Saved: $1,020 in three months

Most people don’t have a spending problem—they have a timing problem. I realized one paycheck carried most of my bills while the other sat idle. I redistributed bills evenly, and suddenly I had $400 “extra” every month.

Saved: $1,200/year (just from rebalancing)

I kept quitting budgeting apps because they made me feel bad. I switched to a paycheck-based system that actually matched how I live—less guilt, more clarity. Once my cash flow made sense, I stopped wasting money “out of stress.”

Saved: Roughly $400/month from fewer “panic” purchases

In 90 days, I wasn’t living with less—I was living with less waste. The best part? I didn’t have to sacrifice anything meaningful.

What I noticed:

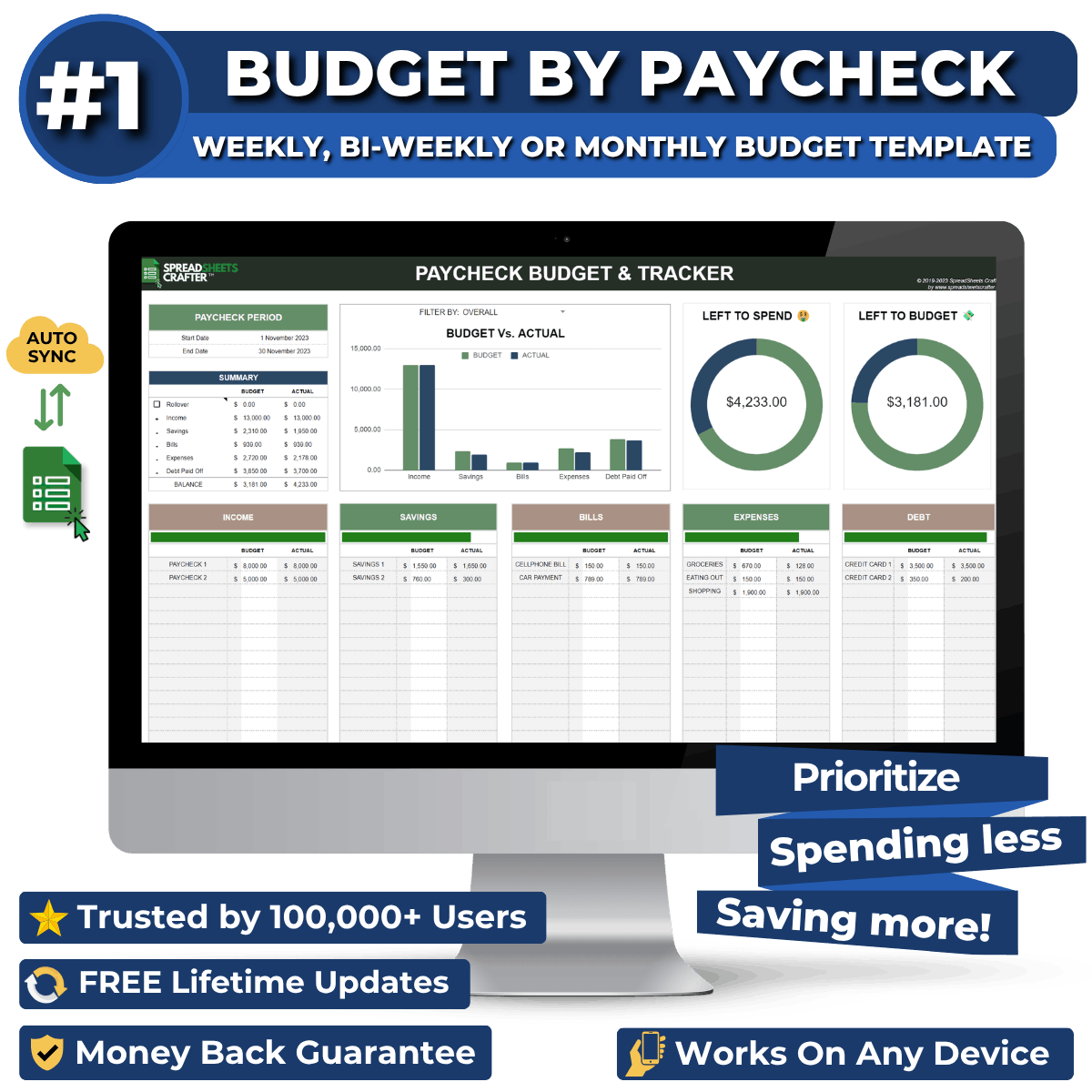

I didn’t track every transaction manually—I used a paycheck-based planner that let me see my money visually, one check at a time.

It’s called Budget by Paycheck, and it’s now the same tool I recommend to all my clients.

Why It Works

It’s not about cutting joy—it’s about cutting waste. My $4,000 proof is the best motivation I’ve ever had.

It’s amazing what happens when your budget finally makes sense.