Your cart is empty

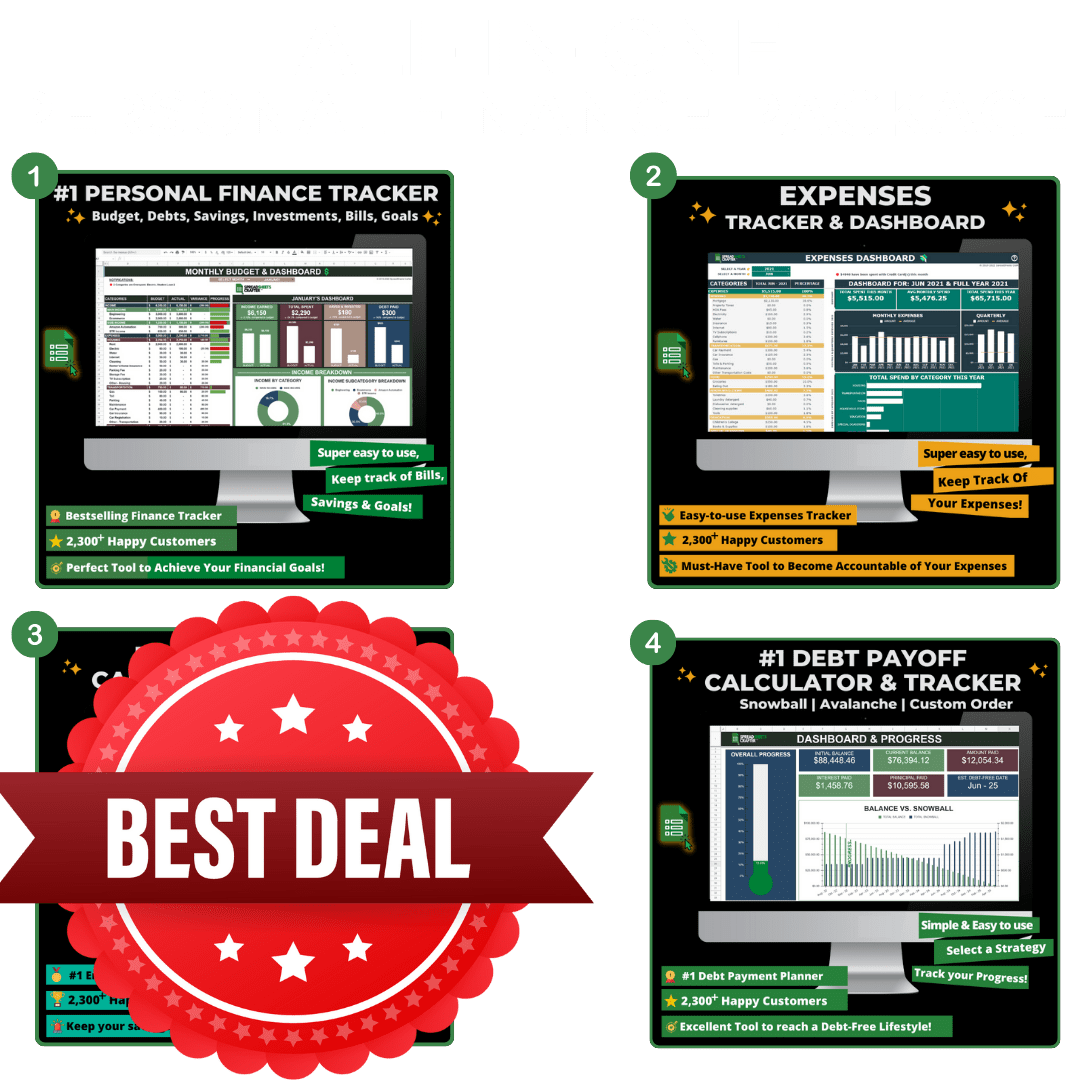

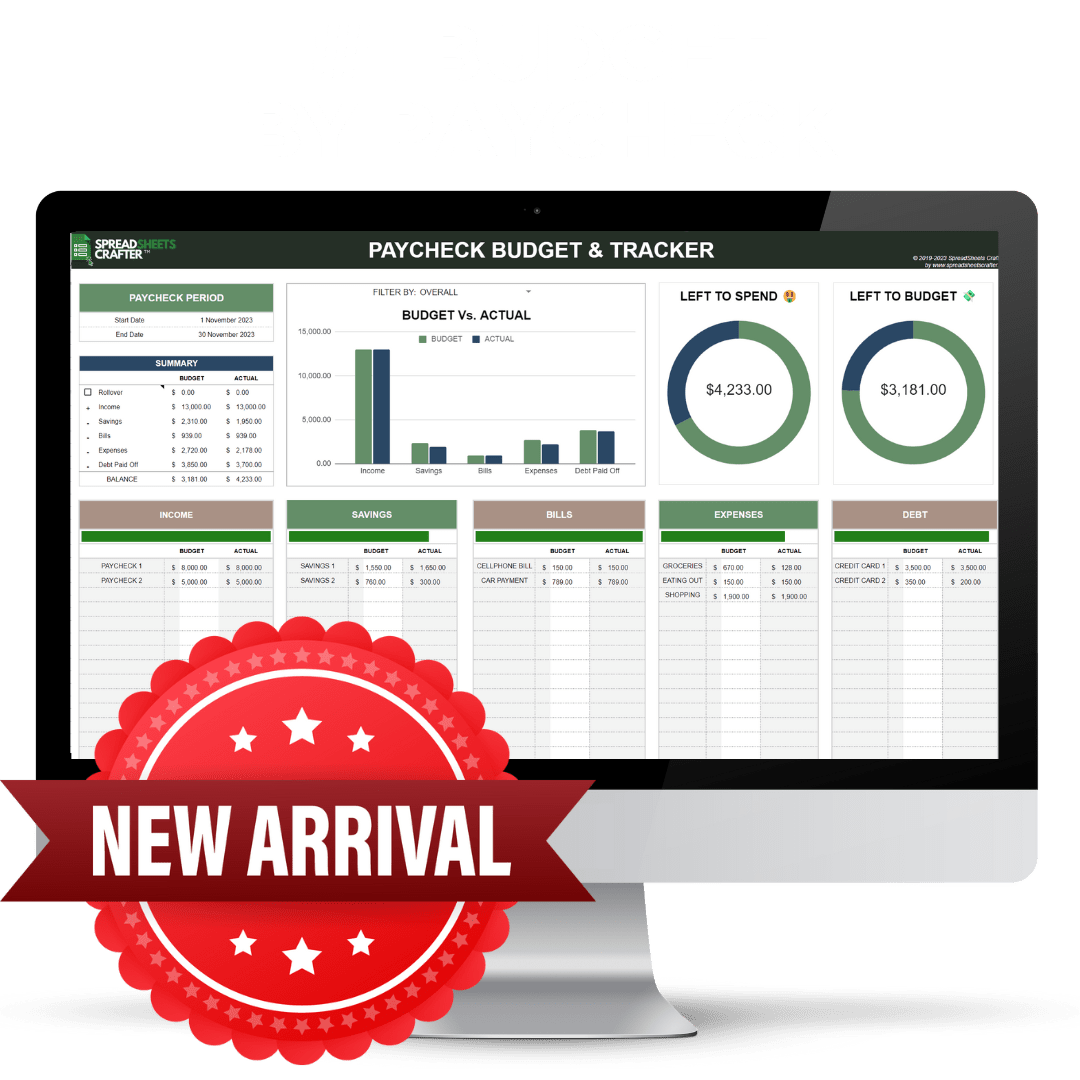

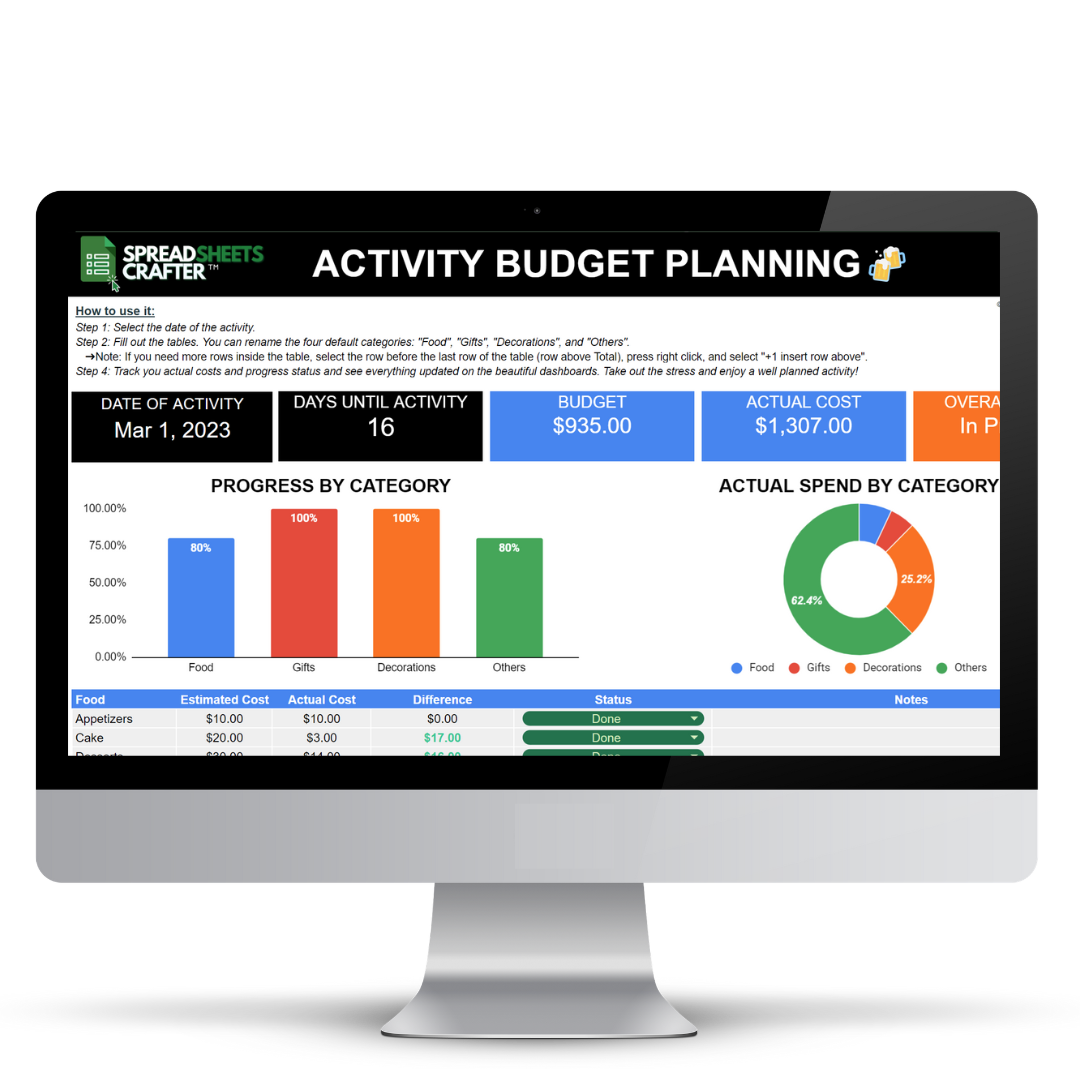

#1 Personal Finance Tracker - Achieve all your Goals with this Easy to use Spreadsheet

476 reviews

Sale priceFrom $29.95

Regular price$74.95

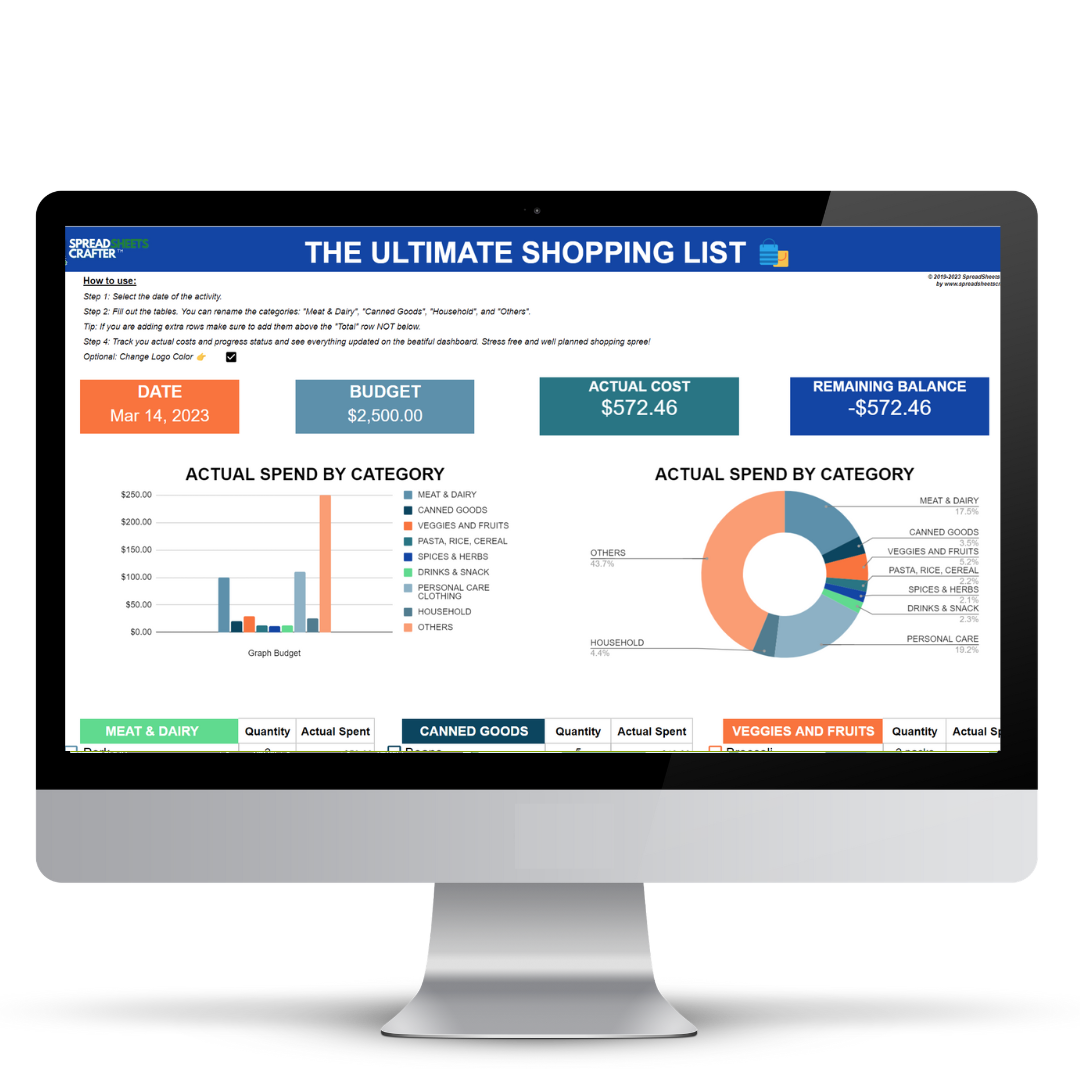

#1 Expense Tracker & Dashboard - Become Accountable of your Spending Habits with this Easy to use Spreadsheet

175 reviews

Sale priceFrom $19.95

Regular price$49.95

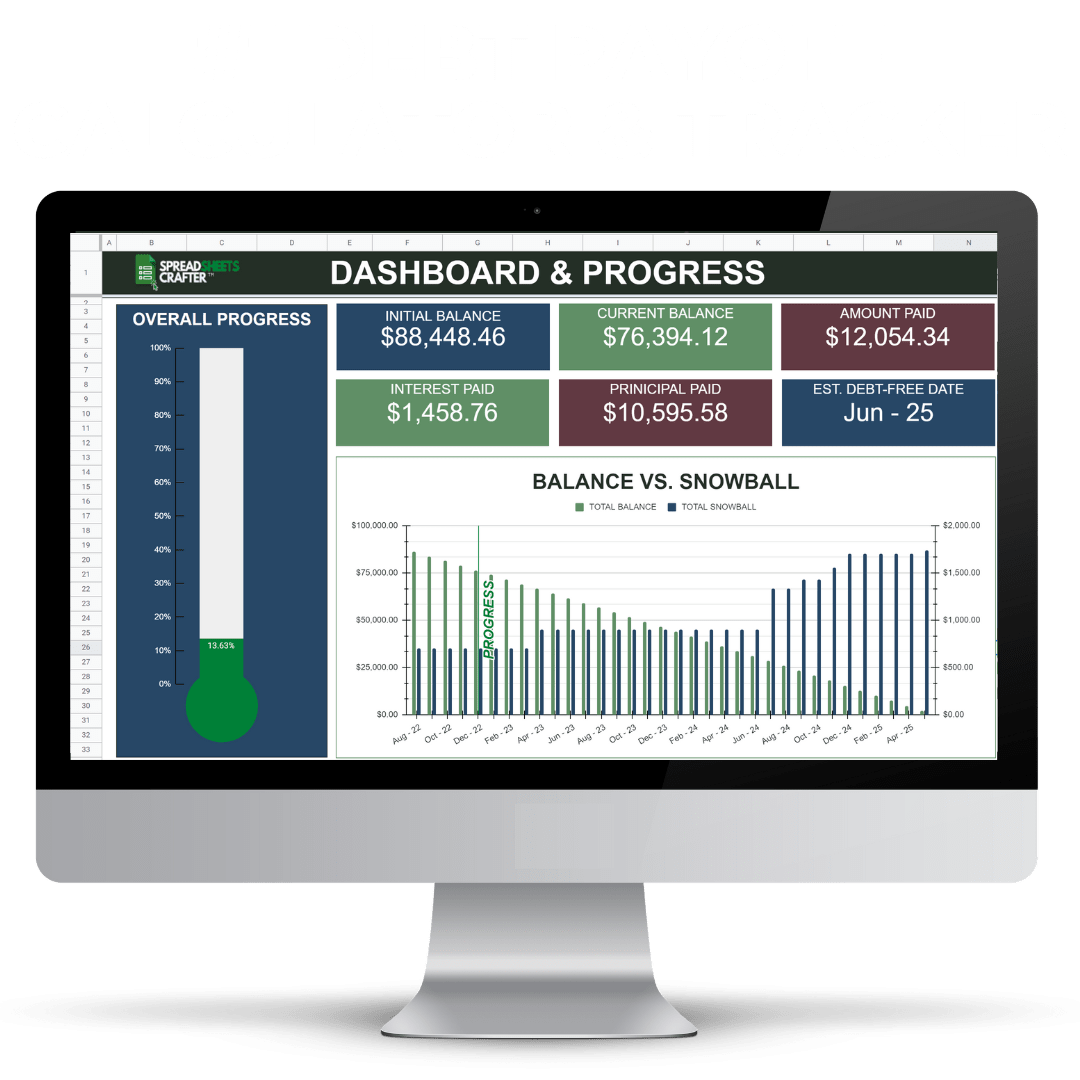

#1 Debt Payoff Calculator & Tracker - Reach a Debt-Free Lifestyle Faster than Ever with this Simple to Use Spreadsheet

228 reviews

Sale price$29.95

Regular price$74.95

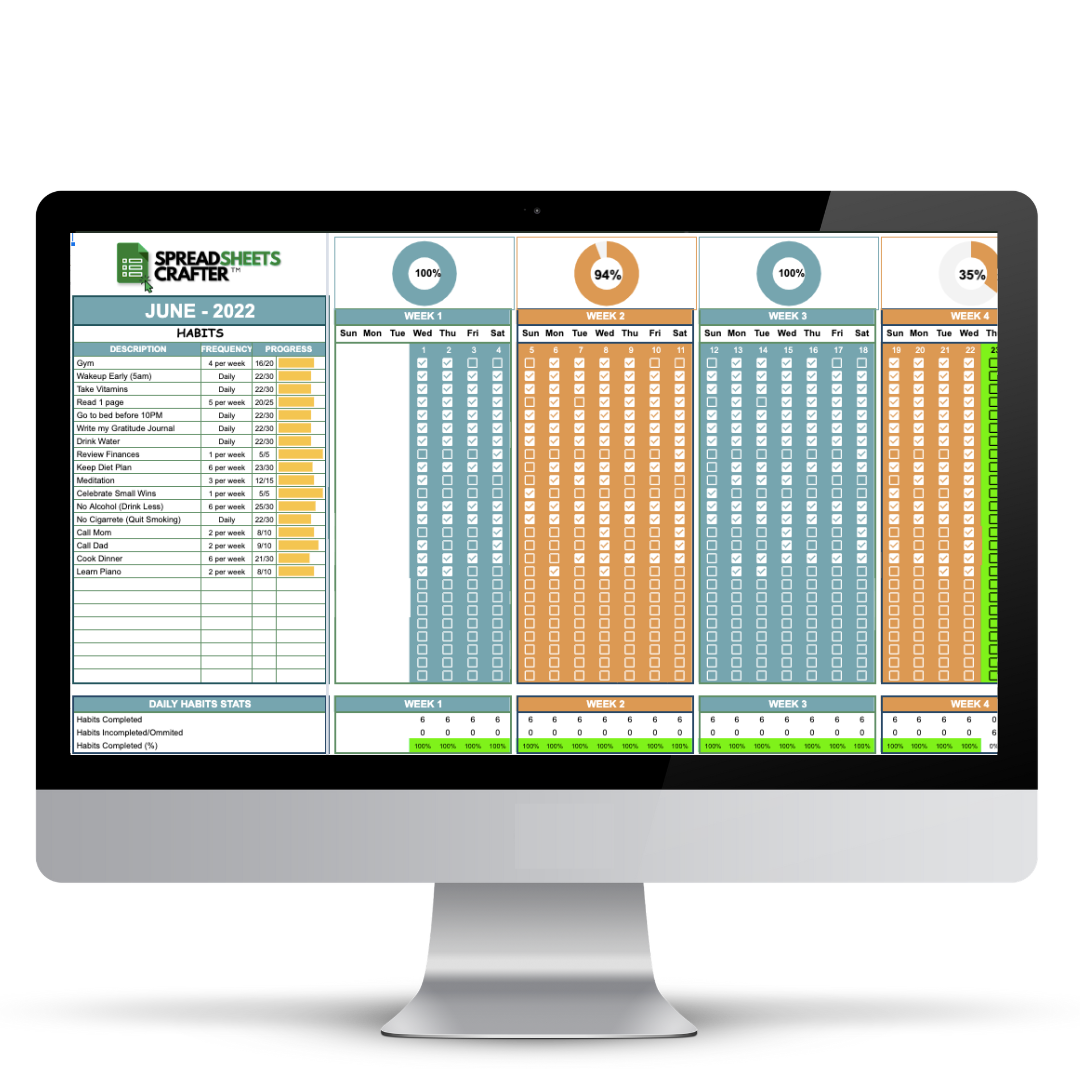

#1 Ultimate Habit Tracker - Improve your Lifestyle with this Easy to use Spreadsheet

256 reviews

Sale price$29.95

Regular price$74.95

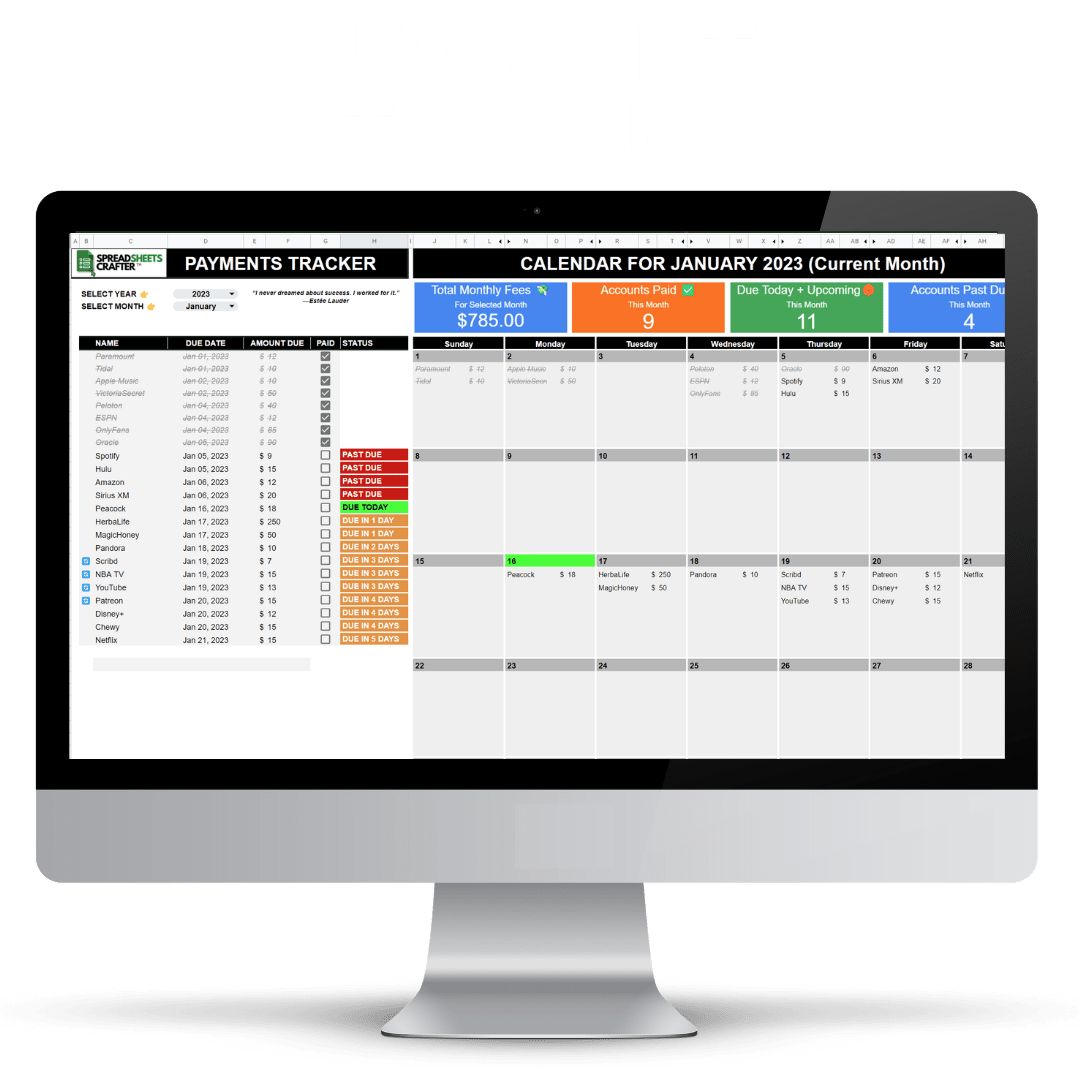

#1 Subscriptions Tracker - Take control of bills and subscriptions and stop paying late fees and overdrafts

212 reviews

Sale price$29.95

Regular price$74.95

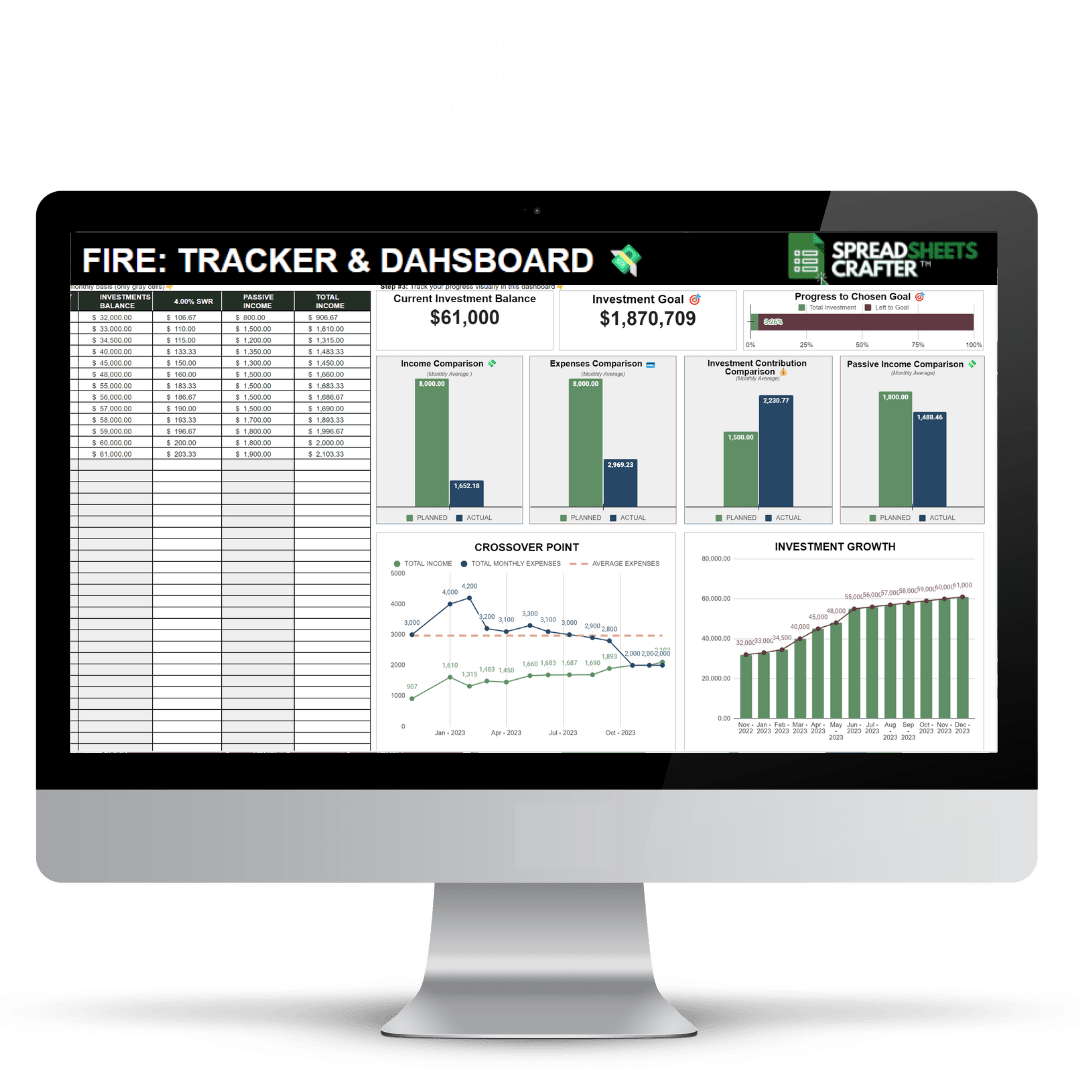

#1 Early Retirement Tracker & Dashboard - Early Retirement Plan

218 reviews

Sale price$29.95

Regular price$74.95