Your cart is empty

Cart

If you’ve ever built a budget and fallen off after two weeks, you’re not broken—your system is.

The truth? Budgeting doesn’t fail because of math. It fails because of design.

After working with hundreds of middle-class families, I found six unusual, psychology-first tricks that actually make budgeting easy to follow—even with real-life bills, kids, and chaos.

I’m Sarah Chen. I’ve been a Certified Financial Planner and Financial Therapist in Seattle for 12 years.

When I tracked what separated my successful clients from the strugglers, six “weird” habits kept showing up. They cut stress, stopped overdrafts, and made saving automatic—without extreme frugality.

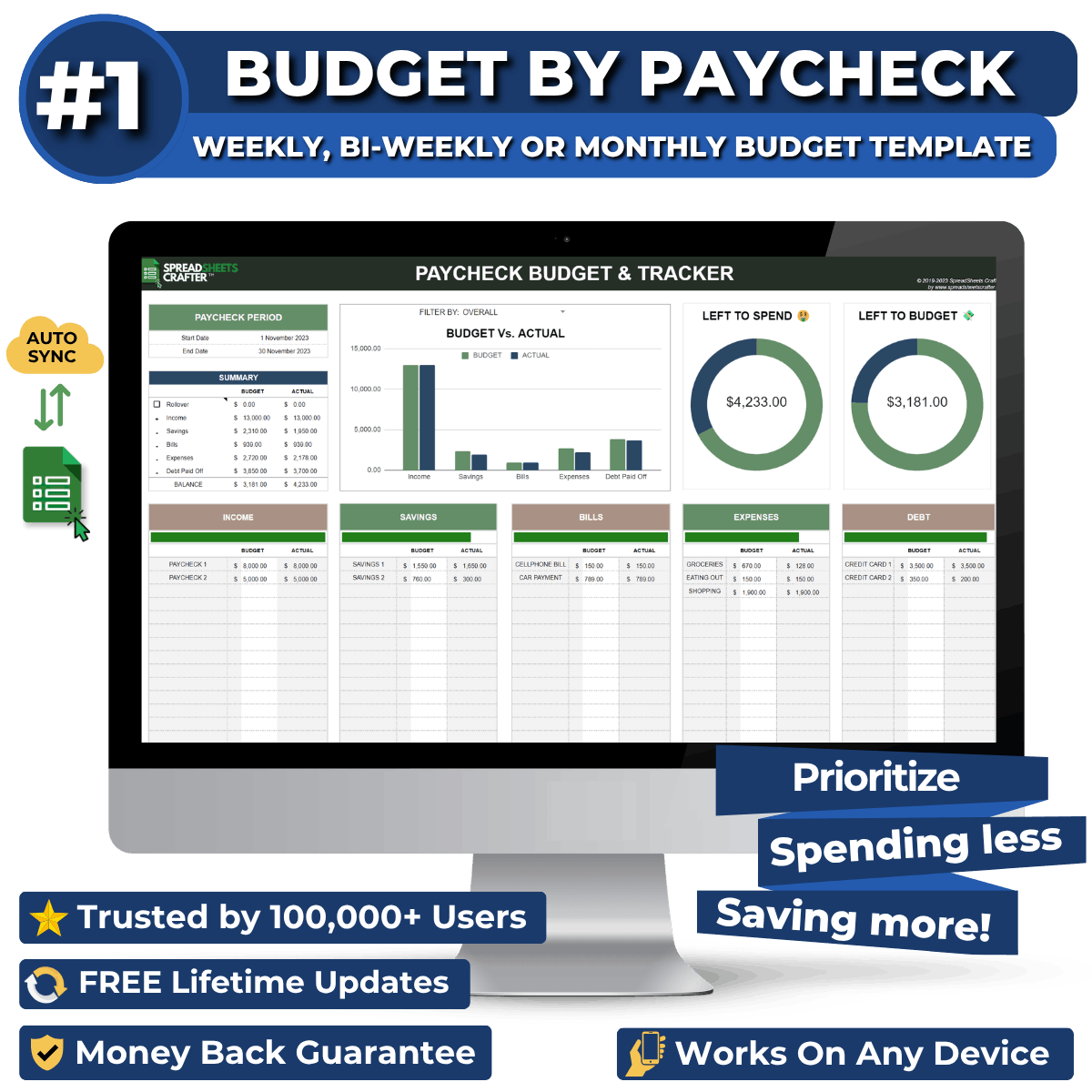

You don’t get paid on a calendar month—so stop planning like you do. Align your plan with your actual pay schedule and assign every bill to a specific paycheck. It kills overdrafts and ends the “too much month, not enough money” problem.

Fast win: Map your next two paychecks and list exactly which bills each one covers.

Before you spend, label each dollar with a purpose (groceries, gas, weekend fun). This simple mental earmarking boosts follow-through dramatically and crushes impulse spending—without feeling restricted.

Fast win: Pre-label $50 of your next paycheck as “guilt-free fun.” You’ll spend less—and enjoy it more.

You don’t need five bank accounts. Use one account, but split it on paper (or in a sheet) into two buckets—one per paycheck. This exposes the #1 hidden issue for high earners: one paycheck is overloaded while the other coasts.

Fast win: If one bucket is drowning, move a bill (see Trick #4).

Call your insurer, lender, or utility and shift a due date into your lighter paycheck period. Most companies allow one or two changes a year. One call can balance your entire month.

Fast win: Move the largest bill that lands in your tightest paycheck week.

People don’t save because they see the money first. Auto-move $25–$50 from each paycheck into a tucked-away savings account you never check. You’ll “forget” it—until you’ve built your first $1,000 cushion.

Fast win: Automate the transfer for the morning your paycheck lands.

Instead of guilt, build permission into your plan. Set a small, upfront “fun” amount each paycheck. When it’s gone, you’re done. This flips your brain from restriction to control—so you actually stick with it.

Fast win: Start with $20–$40. It’s enough to feel good, small enough to keep momentum.

They fix the psychology of money, not just the math: shorter feedback loops, visible cash-flow timing, planned “fun,” and fewer decisions. That’s why people finally stick with them.

What we see after 60–90 days:

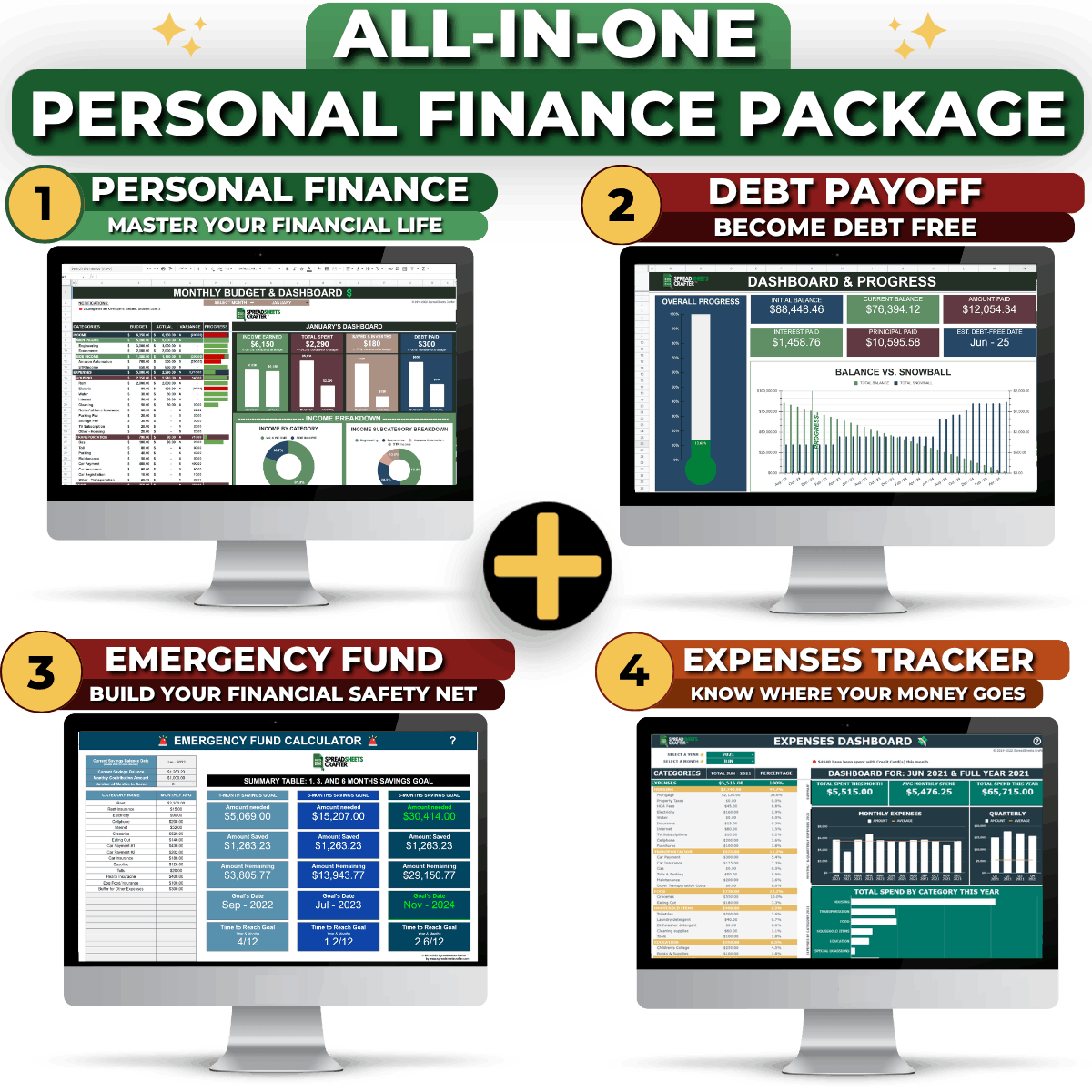

If you want these six tricks built in so you don’t have to think about them, use the Budget by Paycheck system. It plans by paycheck, assigns bills to the right check, highlights overloaded weeks, and keeps the focus on progress—not guilt.

How Budget by Paycheck Implements All 6 Tricks

If you ignore this:

For less than one month of “subscription creep,” you can make these six tricks automatic.

When budgeting fits your real life, it finally works.